Quick Takeaways: TL;DR on Funding Your Career Change

- A coding bootcamp is a career investment, not a cost.

- ISAs are a low-risk option where you pay a percentage of your salary after you get hired.

- Private loans offer predictable, fixed payments and may be a better option if you have good credit.

- Scholarships and grants are free money; you should apply to as many as you can.

- Talk to your bootcamp! They want to help you find a way to pay and can provide the most accurate information on their specific options.

- Never use a high-interest credit card. It’s a surefire way to get stuck in debt.

You’re not here because you’re confused about what a coding bootcamp is. You’re here because you want to know if you can actually afford one without wrecking your finances. Short answer: yes. Let’s get into the how.

This guide is designed to cut through the noise. We’ll break down every single way to pay for a coding bootcamp, tell you exactly what to watch out for, and give you a simple framework to figure out which option is the best fit for your life.

Why Coding Bootcamps Are an Investment, Not Just an Expense

Let’s reframe this from the start. A coding bootcamp isn’t a bill you have to pay. It’s an investment in your future earning potential. You’re not just paying for a class; you’re paying for a career change that can dramatically increase your salary and job prospects.

Most people ask: ‘Can I afford a coding bootcamp?’ That’s the wrong question. The right question is: ‘Can I afford to NOT do this?’

Here’s a reality check with real numbers:

| Scenario | Year 0 Salary | Year 3 Salary |

| Stay in current career | ~$45,000 | ~$49,000 |

| Complete Metana Coding Bootcamp | ~$60,000 | ~$85,000+ |

Coding Bootcamp Financing: ISAs, Loans & Scholarships Explained

You’ve got a lot of choices here, and your bootcamp might not offer every single one. That’s why it’s so important to research your specific school’s policies. Here’s the complete list of options you’ll encounter.

Option 1: Income Share Agreements (ISAs)

ISAs are the rockstar of bootcamp financing. The entire model is built on one idea: the bootcamp only wins if you win.

How it works: You pay nothing upfront. Once you land a job above a minimum salary threshold (say, $50K+), you pay a fixed percentage of your income for a set number of months. No job? No payments.

| ⚡ Pro Tip: An ISA is the best fit if you have little-to-no savings and a low risk tolerance. When the bootcamp’s revenue depends on your job placement, they’re motivated to work hard for you. |

| ✅ Pros | ⚠️ Watch Out For |

| Zero upfront cost | Read the payment cap carefully (e.g., 1.5x tuition max) |

| No payment if you don’t get hired | Watch for forced payment clauses; avoid ISAs with these |

| Coding Bootcamp is incentivized to place you | High earners may pay more total than a loan would cost |

ISAs sound too good to be true, and you should always read the fine print.

- The Payment Cap: There is almost always a cap on how much you can pay back. For instance, the cap might be 1.5x the tuition cost. If the tuition is $15,000, your total payments won’t exceed $22,500. This is a critical detail to check.

- The Repayment Term: The period of time you are required to make payments.

- The Minimum Income Threshold: The salary you must earn before payments begin. A good threshold is one that allows you to live comfortably while making payments.

- Forced Payments: Some ISAs have clauses that require you to start paying even if you don’t have a qualifying job, or they may have a fixed date when payments begin, regardless of your employment status. Avoid these.

Option 2: Private Loans

When federal student loans aren’t available; most bootcamps don’t qualify; private lenders fill the gap. Specialized lenders like Ascent and Climb Credit focus specifically on bootcamp financing and often partner directly with schools.

| ✅ Best for | Good credit history, want predictable fixed payments |

| 💰 How you pay | Fixed monthly installments with interest |

| ⏱️ When payments start | Typically 1–6 months after enrollment |

| ⚠️ Watch out for | Interest accrual, credit score requirements |

| ✅ Pros | ⚠️ Watch Out For |

|---|---|

| Fixed rate = predictable payments | You pay regardless of job outcome |

| May cost less total than a high-earning ISA | Requires a decent credit score |

| Fast approval process with bootcamp partners | Always check total repayment, not just monthly cost |

Option 3: Deferred Tuition

Similar to an ISA but simpler: you pay nothing upfront, then make fixed monthly payments once you land a qualifying job. No income percentage — just a flat payment schedule until tuition is paid in full. Less common than ISAs, but cleaner in structure.

| 📌 Note: Confirm whether there is any interest applied and whether the payment timeline is fixed-term or open-ended before signing anything. |

Option 4: Scholarships & Grants — Free Money

This is the most underused option. Scholarships don’t need to be paid back, ever. Most people assume they won’t qualify and never even apply. That’s a mistake.

Where to find them:

| Source | What’s Available |

|---|---|

| Metana’s own scholarship page | Rolling applications, merit and need-based |

| Women Who Code / Black Girls CODE | Grants for underrepresented groups in tech |

| Course Report & Career Karma | Aggregated scholarship databases |

| Employer diversity funds | Company-sponsored tech upskilling grants |

| ⚡ Pro Tip: Apply to every scholarship you’re remotely eligible for. Many are designed to fill cohort diversity gaps — the bar to qualify is often lower than you think. |

Option 5: Employer Sponsorship

If you’re currently employed, this is the most overlooked path. Many companies offer tuition reimbursement for professional upskilling — and most employees never ask.

| ✅ Best for | Currently employed people with upskilling benefits |

| 💰 How you pay | You may not have to — company covers it |

| ⚠️ Watch out for | Some employers require you to stay for a set period post-training |

Your move: Book a meeting with HR. Frame it as “I want to add skills that directly benefit the team.” The worst they say is no.

Option 6: Military Benefits (GI Bill)

For veterans and active military, the GI Bill covers tuition, housing, and materials. Not all bootcamps are VA-approved — verify Metana’s eligibility directly with the admissions team before making any plans around this.

| ✅ Best for | Veterans and active military personnel |

| 💰 How you pay | You don’t — benefit covers tuition and more |

| ⚠️ Watch out for | Confirm the bootcamp is VA-approved before enrolling |

Read more on veteran and active military benefit cover: the GI Bill

Option 7: Paying Upfront or with a Payment Plan

The most straightforward option — and usually the cheapest in total cost.

| Pay Upfront | Payment Plan | |

|---|---|---|

| Total cost | Lowest — no interest | Higher — installment fees apply |

| Upfront required | Full tuition | Small deposit |

| Monthly burden | None after payment | Spread across 12–48 months |

| Best for | Have savings, want clean slate | Need lower immediate outlay |

| Discount available? | Often yes — ask Metana | Typically no |

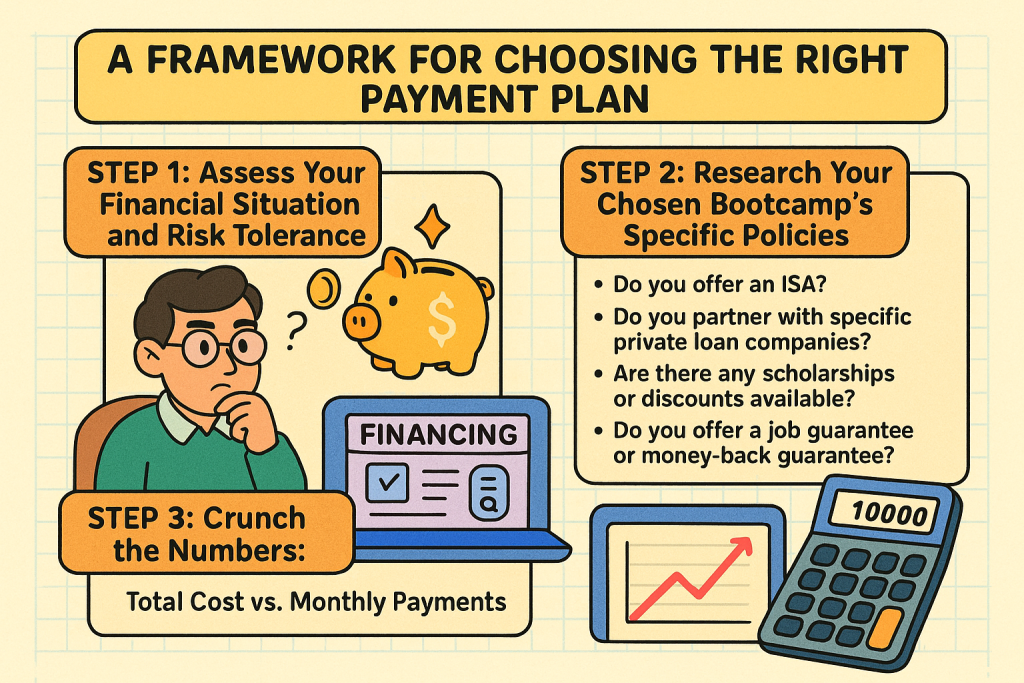

A Framework for Choosing the Right Payment Plan

Okay, you have all the options. Now, how do you decide? Let’s put on our analyst hats and walk through this logically.

Which Option Is Right for You?

| Your Situation | Best Option |

|---|---|

| No savings, low risk tolerance | ISA — bootcamp wins only when you do |

| Good credit, stable income | Private loan — predictable and often cheaper total |

| Currently employed | Try employer sponsorship first, then ISA or loan |

| Military background | GI Bill — verify Metana’s VA approval |

| Strong demographic or academic fit | Apply for scholarships before anything else |

| Have savings, want lowest total cost | Pay upfront — avoid all interest |

Step 1: Assess Your Financial Situation and Risk Tolerance

Ask yourself these questions:

- Do you have an emergency fund? If you have at least 3-6 months of living expenses saved up, you have more flexibility.

- How do you feel about risk? Are you comfortable with the uncertainty of an ISA, where payments could be higher if you land a high-paying job? Or do you prefer the certainty of a loan with fixed monthly payments?

- What’s your credit like? If you have good credit, a private loan might offer a better interest rate than the total cost of an ISA. If your credit is poor, an ISA might be your only option.

Step 2: Research Your Chosen Bootcamp’s Specific Policies

This is non-negotiable. Don’t assume a bootcamp offers all these options. Go to their website, look at their financing page, and even book a call with an admissions advisor. Here’s a checklist of questions to ask:

- Do you offer an ISA? If so, what is the income threshold, repayment term, and payment cap?

- Do you partner with specific private loan companies? What are their typical interest rates and terms?

- Are there any scholarships or discounts available? What are the eligibility requirements?

- Is there a discount for paying upfront?

- Do you offer a job guarantee or money-back guarantee? What are the specific conditions?

Step 3: Crunch the Numbers: Total Cost vs. Monthly Payments

The true cost of each option can be surprising. You need to calculate the worst-case scenario for each.

| Payment Method | Upfront Cost | Total Cost (Example) | Monthly Payment (Example) | Best For… |

| Upfront Payment | 100% of Tuition | $10,000 | $0 | Low-risk, High savings |

| Payment Plan | 10-20% Deposit | $10,000 | $833 over 12 months | Moderate savings, short-term flexibility |

| Private Loan | $0-$500 | ~$12,000 | $200 over 60 months | Good credit, prefers predictable payments |

| ISA | $0 | ~$15,000 (capped) | 10% of salary over 24 months | Low savings, high risk aversion |

Note: These numbers are for illustrative purposes and will vary based on your bootcamp and personal circumstances.

Common Questions About Financing Your Coding Bootcamp

You’re not the first person to have these questions. Let’s tackle a few common ones head-on.

Q: Can I use federal financial aid?

A: No, most coding bootcamps are not accredited like traditional universities, so they do not qualify for federal financial aid programs like FAFSA or Pell Grants.

Q: Are there free coding bootcamps?

A: Yes, some nonprofits and organizations offer free bootcamps, but they are often highly competitive and may have strict eligibility requirements.

Q: Should I use a credit card?

A: A credit card should be an absolute last resort. The interest rates are typically much higher than a private loan or an ISA, which could leave you with a mountain of debt.

The Final Verdict: Making Your Decision and Taking the Leap

Choosing how to pay for a coding bootcamp is a deeply personal decision. There’s no single “best” answer.

- If you are risk-averse and have little to no savings, an ISA is likely your best bet. It puts the pressure on the bootcamp to get you hired.

- If you have a strong credit history and want a fixed, predictable payment schedule, a private loanmight be the smartest financial move.

- If you have the money, paying upfront will save you the most in the long run.

Your goal is to find the option that lets you focus on learning, not on financial stress. Once you have your financial plan, you can stop worrying about the “how to pay” and start getting excited about the “what’s next.” You can also check out Metana’s various bootcamp offerings to find the right fit for your career goals.

FAQs About Coding Bootcamp Payments

Q: What is the average cost of a coding bootcamp?

A: The average cost can vary widely, but most full-time bootcamps cost between $10,000 and $20,000. Part-time or self-paced options are often more affordable.

Q: What is a “money-back guarantee”?

A: A money-back guarantee means the bootcamp will refund your tuition if you don’t find a qualifying job within a specific timeframe (e.g., 6 months after graduation), provided you follow their job-search process. Always read the terms carefully. Some bootcamps, for instance, offer a job guarantee and a risk-free 2-week refund period.

Q: How is an ISA different from a loan?

A: An ISA is a contract to pay a percentage of your future income, while a loan is a contract to repay a fixed amount of money plus interest. With an ISA, you don’t pay if you don’t get a job. With a loan, you’re responsible for payments regardless of your employment status.

Q: Can I get a loan to cover living expenses?

A: Some specialized lenders offer loans that can cover both tuition and living expenses. This is a crucial question to ask when you speak with a loan provider or your bootcamp’s finance department.

Q: Is it possible to get a job with no degree, only a bootcamp certificate?

A: Absolutely. Many companies value practical skills and a strong portfolio over a traditional degree. A bootcamp’s job-placement services, portfolio projects, and interview prep are often what make the difference. Metana’s student success stories and blog posts on career switching provide good examples of this.